Key Takeaways

- Cream Finance is a fork of Compound but offers far more assets to lend and borrow against.

- Though it offers additional features, they are less competitive than the original offerings. The CREAM token also lacks clear utility.

- Cream has proven that the underlying code is secure thanks to an audit from Trail of Bits.

Share this article

Cream Finance takes some of the more popular ideas from DeFi’s lending and borrowing space one step further.

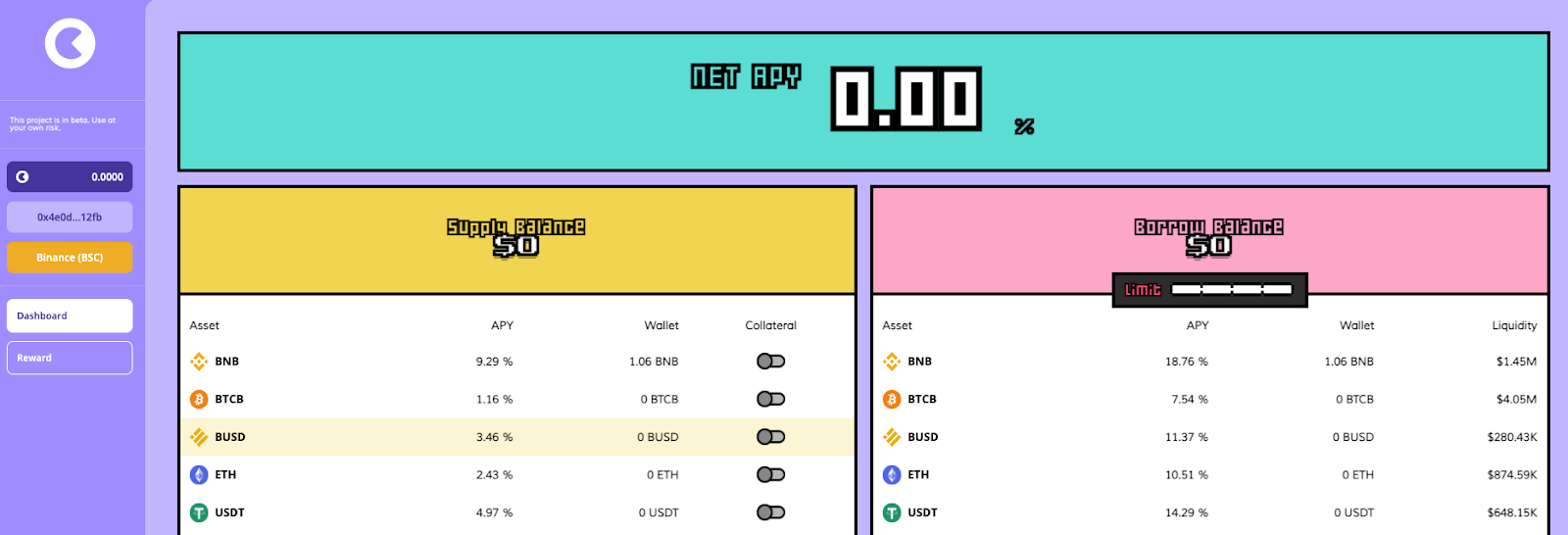

The project lists nearly 70 different assets, LP tokens, and various derivative tokens from many popular DeFi projects. What’s more, users can lend and borrow against each token to create unique opportunities.

Naturally, listing small-cap tokens in this manner comes with a host of risks. As many veterans in the space are painfully aware, small tokens tend to carry much more volatility. When borrowing against such volatile tokens, investors must keep a much closer eye on their loan-to-value (LTV) ratio to avoid liquidation.

It is for this reason that many have called the project a “degen’s playground.”

Still, Cream has done well of late to merge with notable developer communities. The two major attacks the project suffered was also a testament to the strength of its underlying code.

They have separated from an early founder who raised questions about the project’s trustworthiness.

Governance on the platform, however, demands further attention.

The CREAM token, for instance, is tightly distributed to team members, investors, and strategic partners. It is also costly for retail investors to cast on-chain votes on the few issues that do arise.

Re-Introducing Cream Finance

Cream Finance is a fork of Compound, one of the original lending and borrowing platforms.

Since then, however, this particular slice of DeFi has exploded with activity. There are myriad platforms offering users lucrative interest rates on their idle assets. Centralized exchanges such as Poloniex, Bitfinex, Binance, and others have also hopped on board.

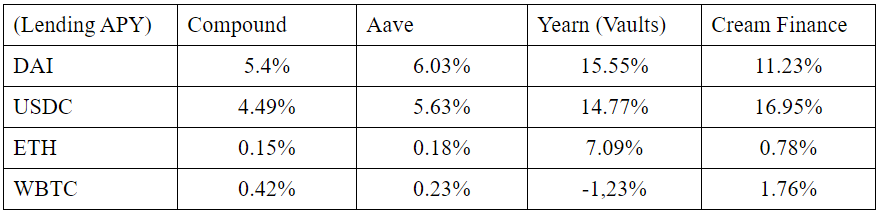

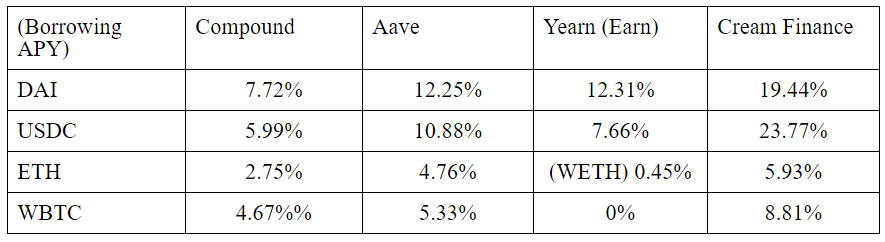

But as these rates fluctuate, so too do users’ interest. Compound, Aave, Yearn, and Cream all offer healthy returns when looking to earn interest in different cryptocurrencies.

Likewise, the rates to borrow certain assets also fluctuate.

If investors only consider this one metric, the best platform is the one where they can earn the most for lending their tokens and where it is the cheapest to borrow. Depending on the asset, Cream may indeed be the best location.

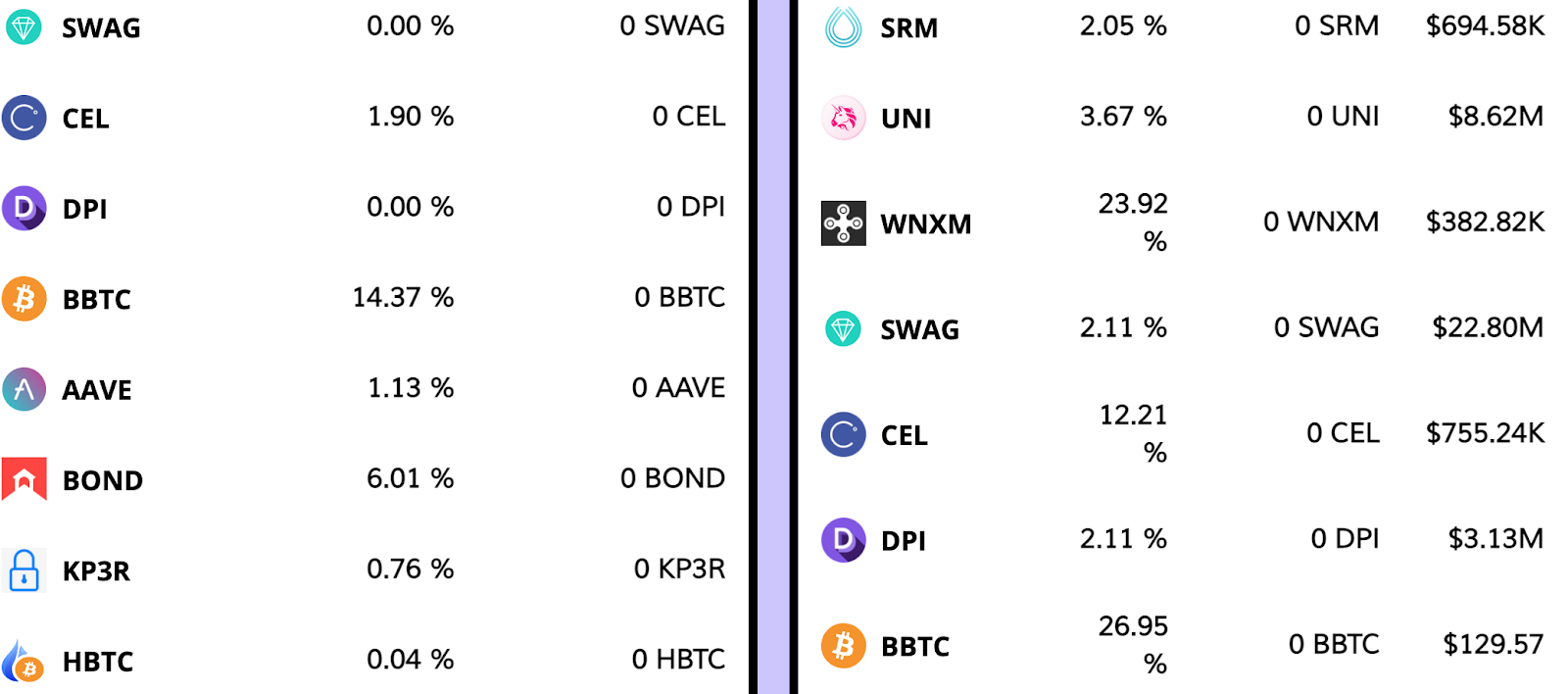

Cream also differentiates itself in this category due to the number of assets it offers. This may be advantageous for yield farmers looking to join a lucrative, though obscure, farm. What’s more, if a farm offers higher rates for a token that the investor doesn’t own, borrowing this token from Cream is not difficult.

Cream has also built an asset swapping platform akin to Uniswap and a Curve-like multi-stablecoin liquidity pool (creamY). It cannot be said that these are necessarily better than the originals, however.

Its greatest value proposition is currently the ability to lend and borrow more exotic DeFi tokens. The platform also lets investors lend and borrow LP tokens for different, popular pairs on Uniswap and Sushiswap.

The Cream Finance Advantage

Cream Finance is all about capital efficiency.

If there is even a slight drop of utility left in an asset, Cream will extract the last few percentages of APY. If a particular token is not deemed safe by Cream’s competitors, investors can be sure that Cream will offer a lending and borrowing market for that token.

To put it simply, Cream is for the advanced investor trying to optimize his investment to the maximum. Naturally, this optimization comes with a host of risks.

The Cream team also firmly believes that the future is multi-chain.

In a call with Crypto Briefing, the current project lead Leo Cheng explained that the company’s objective is to build wherever there are users. Porting different versions of Cream on other Ethereum Virtual Machine (EVM) compatible chains can only be a good thing, especially when fees on Ethereum are so high.

Everything about Cream is catered to investors.

The swap fees are a low 0.25%, and the protocol supports far more assets than competitors such as Compound. What’s more, the platform hosts a larger array of more exotic cryptocurrencies. Interested users can, for instance, lend AKRO and borrow FRAX in exchange.

Cream started as a fork of Compound and distributed a sizable amount of its governance tokens to the Compound team, which has led to a very amicable relationship between the two projects. Compound CEO Robert Leshner and Compound Labs have been named as Security and Technical advisor earlier. Leshner also holds one of the keys to the CREAM multisig

Cream has also merged with Yearn Finance, another one of the most-talented teams working in DeFi at the moment. Together, they launched the Iron Bank.

Iron Bank solves one of the foremost issues of DeFi, the need to overcollateralize any peer-to-peer loan. Through Iron Bank, protocols can borrow from other protocols with next to no collateral. As Cream noted in the announcement:

“In traditional finance, the peer-to-peer lending market size is around $70 billion in loans outstanding. That is a pittance when compared to the size of all US corporate debt which at year-end 2020, soared past $10 trillion.”

Protocol-to-protocol lending has the potential to be one of the biggest DeFi markets in the future.

As protocols replace companies, the market for loans between those protocols could certainly overtake peer-to-peer lending volume. Solutions like Iron Bank offering zero-collateral lending will be an important part of the future financial system.

Project’s Shortcomings

Possibly the most important intangible resource any business has is its reputation. This counts double in DeFi.

Open-source code and ease of launch often mean that a protocol that has seen too many failures or hacks is often forgotten by investors as they move liquidity elsewhere.

It is a testament to the resilience of Cream Finance to see they’re still around after what can only be described as a chaotic history.

The first issue has been the hacks.

In February, Alpha Finance and Cream were targeted by one of the most lucrative hacks in the history of DeFi: a flash loan attack that cost both protocols $37.5 million. The hackers exploited a loophole in Alpha Finance’s code and managed to borrow from the Iron Bank protocol.

A different hack compounded this bad news on Mar. 16 when Cream’s website was compromised. Hackers managed to take control of the DNS and request users’ seed phrases from the website’s UI. However, after talking with Cream’s project lead, the Crypto Briefing team has been notified that no user had come forward claiming they got tricked and lost funds.

While these two hacks are serious matters, the silver lining is that Cream’s own smart contracts were never compromised. In the first case, the loophole was on Alpha’s side, and in the second, only the website’s DNS was exploited, not the actual contracts.

Another issue that deserves to be raised with Cream has to do with the CREAM token.

The token has two uses: governance and capturing some of the fees spent on the platform. However, decisions left to governance have been few and far between. The amount of fees the platform receives is also relatively low.

Governance is a tricky subject for Cream. Under the leadership of its previous CEO Jeffrey Huang (also known in the entertainment industry as Machi Big Brother), Cream didn’t offer many community governance opportunities.

But during the merger with Yearn Finance, Huang left Cream, and with that departure, a more open governance system has taken shape.

Still, a few rules remain problematic to achieving this new vision.

For instance, to propose a vote, individuals must hold 1,500 CREAM tokens, which represents more than $160,000 at the time of writing.

It must also be noted that the importance of governance in different protocols can vary strongly.

Compound, for example, is by design quite limited in the application of the protocol and the decisions in which the community can participate. Synthetix is heavily-driven by community governance, which can be seen by the frequent synthetic offerings rolled out. Apart from new listings, Cream doesn’t necessitate community governance as much as other DeFi platforms. Its Discord is nonetheless quite active, with power-users suggesting changes to the core dev team daily.

The final issue with the CREAM token is its distribution. While originally 9 million tokens were released, 6 million of these were burned in September. This leaves the team, investors and advisors, and Compound, a strategic technology partner, with 38.5% of the supply of CREAM. This leaves the community with 1.8 million tokens, distributed as LP rewards over the next few years.

Another issue that has tarnished Cream’s reputation is the lack of an audit, as the Cream team led by Huang didn’t believe an audit was necessary. The new management has quickly taken the necessary steps to fix this issue and announced on Mar. 1 they received an audit from Trail of Bits.

Another issue that remains is that Cream does rely, if only in small part, on its own oracle. According to the audit report, though this use is limited. They write:

“C.R.E.A.M. v1 is now using decentralized oracle services across 81% on Ethereum and 94% on Binance Smart Chain. C.R.E.A.M. v2 Iron Bank has integrated decentralized oracle services across 77% of our markets. We are working toward 100% coverage by decentralized oracles. Specifically, we are focused on moving all oracles in C.R.E.A.M. Finance to decentralized options such as Chainlink and Band Protocol.”

Oracles are used to determine certain variable factors that are important in the calculation of lending and borrowing parameters and liquidations. Oracle-based attacks have been central in high-profile hacks which use flash loans to exploit the vulnerabilities of centralized oracles. Decentralized oracles are expensive, but they are an important security measure, providing stronger protection against these types of attacks.

Getting Started

Cream Finance allows users to maximize yield on their tokens. Compared to a platform like Aave, Cream focuses on capital efficiency to bring the most out of a wider variety of tokens.

Here is an example of a yield optimization strategy on Cream and why it would yield better results than other DeFi platforms.

- Stake USDT in Cream for yield, lending the token to potential borrowers.

- Receive crUSDT token, representing the stake in the Cream/USDT pool.

- Stake this crUSDT token in a creamY pool, Cream’s native AMM platform, to receive part of the swap fees of people exchanging in the USDT-crUSDT liquidity pool.

- Receive CREAM tokens for providing liquidity in this pool.

Every activity in this strategy happens within the Cream ecosystem. Users can lend their capital on a platform like Aave or provide liquidity on a decentralized exchange like Uniswap. But Cream users can do both on one platform and receive CREAM tokens each step of the way.

Cream Community

Cream Finance launched in August 2020 under the leadership of Jeffrey Huang. A serial entrepreneur in crypto who was responsible for the Mithril project. He also has various investments in Taiwan’s entertainment industry, including a hip-hop band, new media, and an e-sport team.

A big supporter of the Binance Smart Chain, he was one of the reasons why Cream was one of the first projects to launch on BSC in September.

Huang is an interesting character, to say the least, but his departure from Cream is good news for the protocol.

He was linked to several projects which were linked to voting manipulation and exit scams.

Under his tenure, the Cream Finance team worked closely with the Compound team (from which Cream is a fork). This partnership has continued, leaving Cream close to one of the top developer teams in the DeFi space. At the time of the Yearn merger, Huang left the project.

Close proximity with such talented developer teams benefits Cream’s code and its potential for partnerships with other major players in the DeFi space.

Add to that a growing community on Discord and, provided Cream Finance manages to meaningfully include its users in governance, the future of the Cream community is bright.

This news was brought to you by ANKR, our preferred DeFi Partner.

Share this article

All You Need to Know About DeFi’s SushiSwap Saga (But Were Afrai…

The SushiSwap saga and its native token, SUSHI, will go down in crypto history. What began as a tokenized version of Uniswap has spiraled into something much more. It reminds…

What is Dogecoin?

So what is the story behind DOGE? How did it become the asset of choice for a group of anti-establishment retail traders in January 2021, and what are the chances…

Cream Finance, PancakeSwap Websites Compromised

DeFi protocol Cream Finance is experiencing its second hack of 2021. This time, attackers have targeted the website’s DNS and are using it to request users’ private keys and seed…

DeFi Project Spotlight: yEarn.Finance, the Ultimate Yield Farming Mach…

yEarn Finance has quickly become one of the most popular DeFi protocols in 2020. It brings together many of the disparate tools, platforms, strategies, and tokens from throughout the ecosystem….