Decentralized finance doesn’t seem so decentralized after all, especially when looking at token concentration.

Key Takeaways

- 90% of the supply for most DeFi tokens is held in less than 10% of addresses.

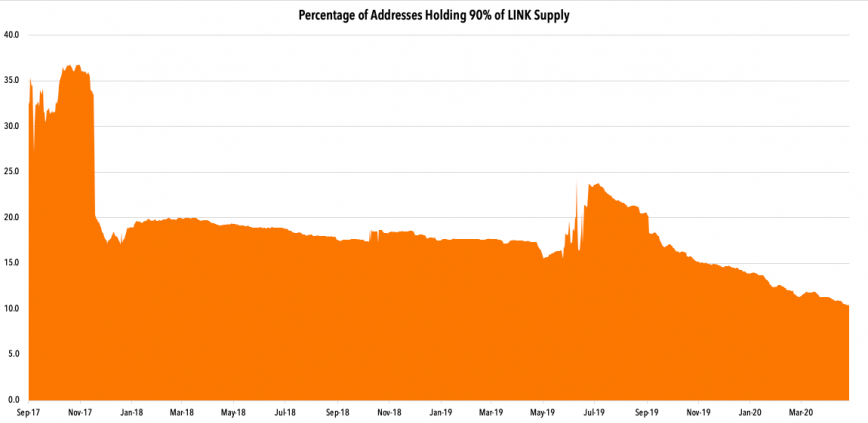

- LINK is the least concentrated of the analyzed coins, as the token’s investor base expanded as it experienced price appreciation.

- MKR’s supply is concentrated in less than 1% of all addresses, jeopardizing its token-based governance model.

- Utility token concentration is a result of bootstrapping adoption and high conviction whales doubling down on their bets.

The DeFi news category was brought to you by Ampleforth, our preferred DeFi partner

Share this article

Token supplies for top DeFi protocols are centralized among a tiny fraction of super-wealthy holders. Chainlink, Kyber Network, MakerDAO, 0x Protocol, and Bancor all have worrying levels of token concentration. For some of these protocols, this could prove disastrous.

Analyzing Supply Concentration

Chainlink, Kyber Network, MakerDAO, 0x Protocol, and Bancor are a few of top names in the popular niche of DeFi. These protocols have collectively seen immense growth since 2019. While the end goal of these protocols is to decentralize financial systems, their tokens are highly concentrated in the belly of whales, imperiling this goal.

There’s a similar trend with all five of these protocols: coins are well spread out across several addresses after the initial token sale. But after some time—usually a few weeks or months—tokens start to accumulate in a few addresses.

Two months after the LINK ICO, 35% of addresses accounted for 90% of the LINK supply. The concentration of LINK consistently increased, with 15-20% of addresses for most 2018 and 2019. As of May 2020, 11% of LINK addresses held 90% of LINK tokens.

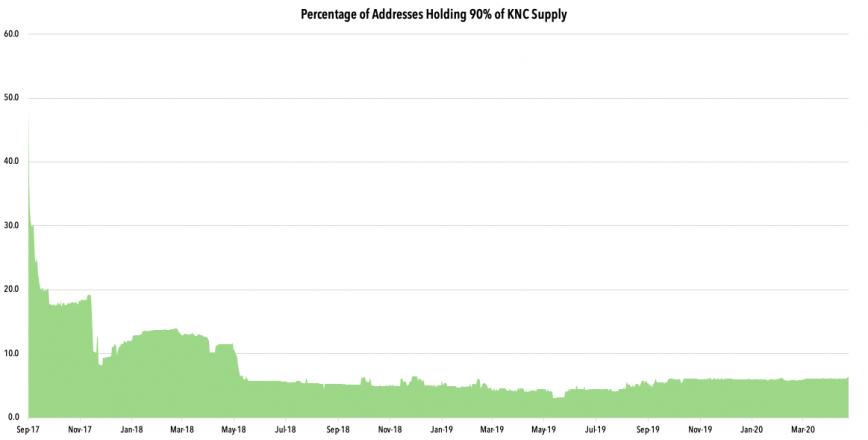

For Chainlink (LINK), the concentration of tokens is lower than the others, which is arguably a byproduct of its massive price appreciation drawing in new investors. Kyber Network’s (KNC) token supply has almost always been with a few whales, with the 90% of KNC supply resting in less than 10% of addresses since May 2018.

Kyber didn’t have explosive price appreciation like LINK until 2019. Since then, more investors have entered KNC positions, causing the 90% concentration measure to halve from a low of 3% to 6% of all KNC addresses.

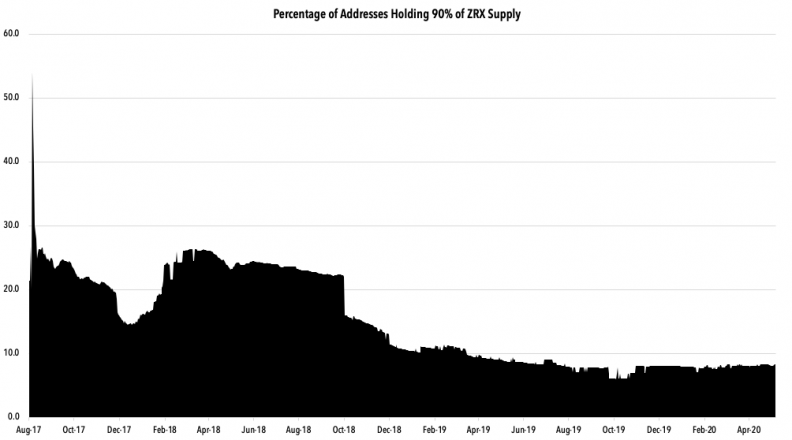

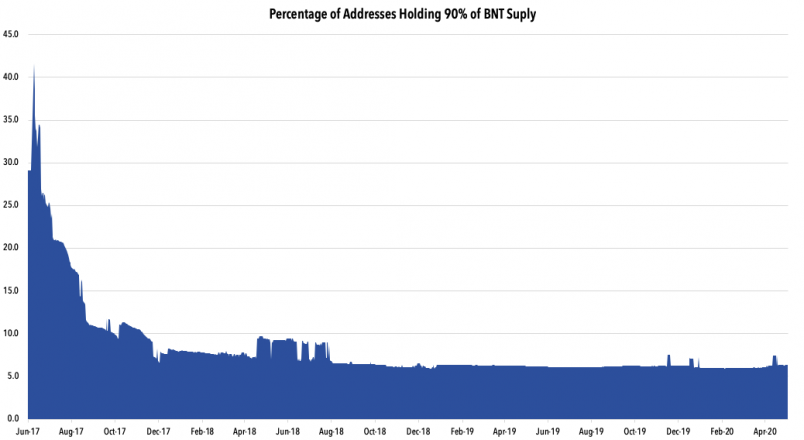

Bancor (BNT) and 0x Protocol (ZRX), which are liquidity routers like Kyber, are in a similar boat with 90% of BNT and ZRX supply sitting in 6% and 8% of total addresses respectively.

For ZRX, this measure was as high as 25% between Feb. 2018 and Oct. 2018 as the token saw manic pumps.

BNT, on the other hand, has seen steady supply centralization with less than 10% of addresses holding 90% of tokens since late 2017.

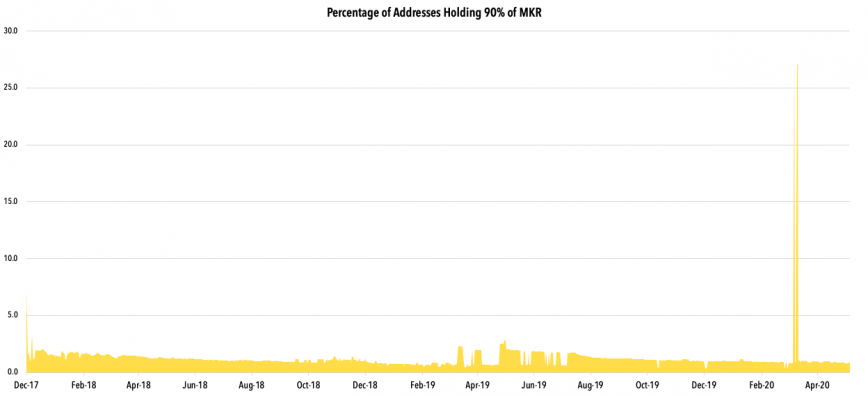

The most concentrated DeFi token, by and large, belongs to MakerDAO (MKR). For most of the token’s life, less than 1% of total MKR addresses held over 90% of the supply.

There were, however, a few anomalies after the infamous Black Thursday event, causing MKR supply distribution to rise. Between Mar. 12 and 17, 25% of total MKR addresses held 90% of all MKR.

Blaise Cavalli, co-founder and CEO of Nyctale, commented on this anomaly, believing it to be a result of “the emission of new tokens that they [MakerDAO] had to perform to maintain the value of the DAI, after some issues in their on-chain liquidation mechanism.”

Maker announced their intention to recoup network losses by selling fresh MKR on Mar. 12, but the auction went through on Mar. 19. The date range for the anomaly conveniently slips in between these two dates, which supports Cavalli’s theory.

Token Concentration Isn’t Always Bad

Utility tokens tend to accrue to users that actively support the network. For nascent networks that are still grappling with adoption, the number of operators on the network is limited. The token supply tends to flow to these few operators, who distribute it based on their investment thesis and demand from market participants. Token concentration is a direct result of new tokens accruing to these few users.

Just like BTC supply is directed at users that secure the network through mining, Chainlink node operators receive LINK for acting as data oracles. Kyber reserve operators are paid in KNC to provide liquidity.

Excluding network operators, whale accumulation has always been a sign of bullish momentum in crypto, as long-term accumulation reduces supply in the open market, thereby applying upward pressure on prices. High conviction whales also contribute to token concentration.

This narrative holds for ChainLink, Kyber, 0x, and Bancor, all of which are utility tokens. Maker (MKR), however, is a different story. Since MKR is a governance token used to participate in executive votes on the MakerDAO, concentration means that a small number of participants can control the proposals and the direction the protocol takes.

The concentration of supply for any governance token puts the decentralization of the protocol at risk.

Most utility tokens offer no control over the protocol—at least, not without a DAO that facilitates token voting. Governance is instead largely community-driven, albeit these communities are still tiny, making some degree of centralization inevitable.

The token concentration phenomenon can be seen in most crypto networks and subduing it will occur organically as more investors and active network participants come along. But governance tokens require widespread distribution across a number of stakeholders to safeguard these networks from centralized control.

This data was made available through Nyctale’s open data initiative.

The DeFi news category was brought to you by Ampleforth, our preferred DeFi partner